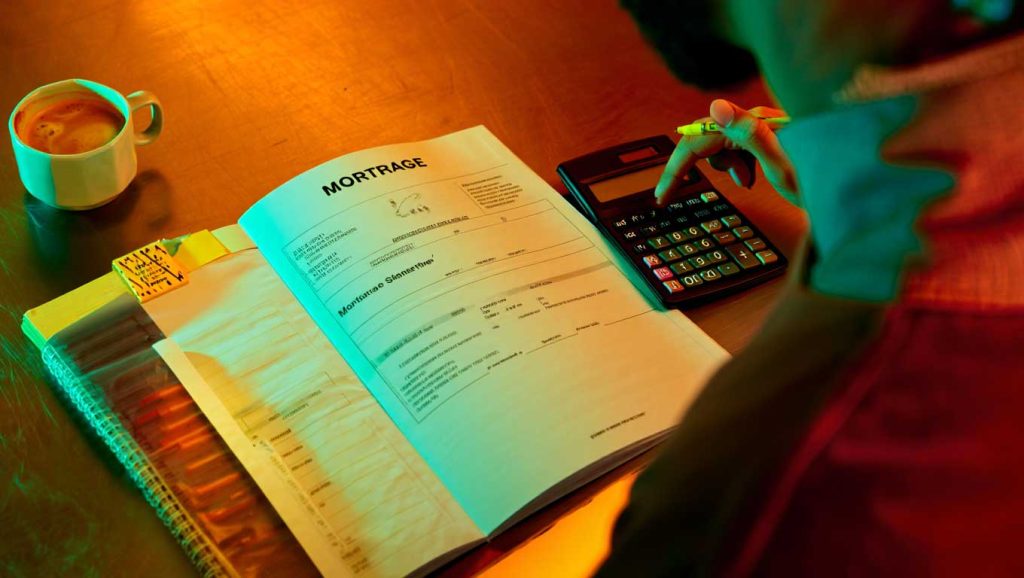

Your monthly statement isn’t routine paperwork, it’s a dashboard of emerging risk. Rising payment amounts, escrow swings, or new fees can foreshadow delinquency or rate shocks in the months ahead.

The quiet number on page one that suddenly changed

Powerball winner scoops $1.817 billion on Christmas Eve, what happens next will change their life forever

Zendaya shuts down pregnancy rumors after viral London outing with Tom Holland goes too far—here’s what she actually said

Watch for an unexplained jump in “Total Amount Due” or an “Explanation of Amount Due.” Under federal rules, periodic statements must itemize principal, interest, and fees—if those lines move, something changed in your loan, escrow, or charges.

Escrow “shortage” or “deficiency” flags often land here first and can trigger catch-up payments. A surprise increase usually means higher taxes or insurance, or a reduced cushion after analysis.

Who sleeps easier—and who’s exposed to the next shock

Arkansas lottery wins $1.817 billion Powerball jackpot on Christmas Eve, here’s what happens to the money

Powerball winner scoops $1.817 billion jackpot on Christmas Eve, but nobody knows who they are yet

Fixed-rate borrowers with stable escrows tend to have fewer surprises, while adjustable-rate and government-backed borrowers may see larger swings when taxes, insurance, or interest reset.

“Average monthly payments increased nearly 46% and exceeded $2,000 per month.” — Rohit Chopra, Director, Consumer Financial Protection Bureau.

If your statement starts listing late fees, suspense-account movements, or repeated past-due notices, that’s a sign to act early—before hardship spirals.

The exact moves you need to stay safe

Use your statement to run a quick prevention plan. Do these steps in order:

| Step | Detail | Deadline |

|---|---|---|

| 1 | Compare “Amount Due” vs last three statements; note any fee or escrow jumps | Within 48 hours of receipt |

| 2 | Call servicer about any new fee codes, escrow shortage, or interest-rate change | Within 7 days |

| 3 | Request loss-mitigation options if payment is unsustainable (forbearance, mod, refinance) | Before next due date |

| 4 | Audit taxes and insurance; get competing quotes and verify assessments | Within 30 days |

Keep the PDF of your statement; it’s accepted documentation when you dispute errors or request help. Track the delinquency clock—30/60/90 days past due thresholds escalate fees and foreclosure risk.

The @CFPB is hearing from homeowners about unscrupulous debt collectors attempting to pursue “zombie” mortgages past the statute of limitations. https://t.co/SkCL4EK7H8

— Rohit Chopra (@ChopraUSA) August 2, 2024

What could surface in the next 30–90 days

Expect escrow re-analysis letters that adjust your monthly payment, especially during annual tax or insurance renewals. If you’re on an ARM, watch for the first post-teaser adjustment—higher indexes can push payments up sharply within 30–90 days of a reset notice.

National delinquency stats can move even when the economy looks stable; if your region’s rates tick up, servicers may tighten timelines. Use that time cue, act before the next due date to avoid rolling late fees.

The line item everyone is eyeing—are you reading it right?

Are you overlooking a small line that signals big trouble—like “partial payment held in suspense,” “corporate advance,” or a new “escrow shortage payment”? Those are early alarms. Have you compared your principal reduction month to month to confirm amortization is on track?

If your “Projected Payments” box shows bigger escrow draws for taxes or insurance, do you have a plan to cushion the hit before it lands?

When struggling homeowners can get the help they need without unnecessary obstacles, it’s better for borrowers, servicers, and the economy. The @CFPB has proposed rules to reduce avoidable foreclosures and make the mortgage market more resilient.

https://t.co/jbUIbNksS4— Rohit Chopra (@ChopraUSA) July 10, 2024

SOURCES

- https://www.consumerfinance.gov/rules-policy/regulations/1026/41

- https://www.consumerfinance.gov/rules-policy/regulations/1024/17

- https://www.mba.org/docs/default-source/research-and-forecasts/members-only-research/nds-q225-report-summary-final.pdf

Jessica Morrison is a seasoned entertainment writer with over a decade of experience covering television, film, and pop culture. After earning a degree in journalism from New York University, she worked as a freelance writer for various entertainment magazines before joining red94.net. Her expertise lies in analyzing television series, from groundbreaking dramas to light-hearted comedies, and she often provides in-depth reviews and industry insights. Outside of writing, Jessica is an avid film buff and enjoys discovering new indie movies at local festivals.

I remember my uncle once said, Watch out for those hidden numbers in contracts, theyll get ya. Now, those cryptic mortgage notices make me wonder what else is lurking in the fine print. Gotta stay sharp, folks.

Man, those mortgage notices are like cryptic warnings, hinting at financial doom. Its like deciphering ancient hieroglyphics, trying to figure out what hidden risks lurk in the fine print. Sneaky numbers on page one can make or break ya!

Dude, I feel ya! Those mortgage letters are like the Da Vinci Code of finance, but with way less Tom Hanks running around. Its a total mind game – one wrong move and bam, financial disaster! Who knew numbers could be so sneaky, right? Its like theyre playing poker with our wallets and we dont even know the rules. Crazy stuff!

Man, those sneaky mortgage notices playin hard to get with the real deal. Gotta decode that page 1 number like its the Da Vinci Code, or else watch out for the financial rollercoaster ahead. Time to crack the safe!

I once ignored those boring numbers on my mortgage notices, until one day it hit me like a ton of bricks. Now, Im all ears for that quiet number on page one, ready to tackle the financial rollercoaster head-on.

Man, those mortgage notices are like a cryptic message, warning bout financial doom. Gotta decode that hidden number on page one before its game over. Whos brave enough to face the music and take the right steps?

Man, those mortgage notices are like a cryptic message warning of impending doom. The quiet number on page one? Its the ticking time bomb, waiting to screw us over. Gotta decode those signs before its too late!