One unchecked HELOC or second-lien “consent” clause can derail your refinance in days, not weeks. If the junior lender refuses to resubordinate, your closing stalls and your rate lock can expire, costing you real money.

The clause that flips your refinance if a HELOC is on title

Powerball winner scoops $1.817 billion on Christmas Eve, what happens next will change their life forever

Zendaya shuts down pregnancy rumors after viral London outing with Tom Holland goes too far—here’s what she actually said

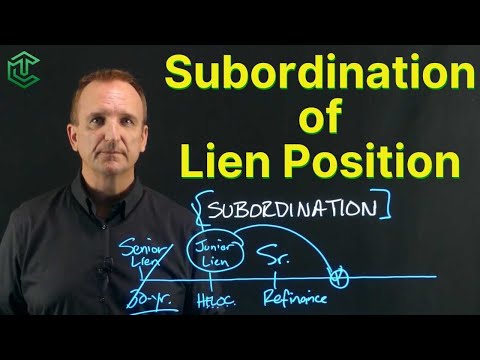

When you refinance with a home equity loan or line of credit still open, the junior lender must agree to “resubordinate” behind the new first mortgage. Without that written consent, the new loan cannot take first position and the deal can collapse.

This risk is often invisible in disclosures until the title report surfaces existing junior liens and the refinance lender requests subordination from your HELOC or second-mortgage servicer.

Why some homeowners feel safe while others hit a wall

Arkansas lottery wins $1.817 billion Powerball jackpot on Christmas Eve, here’s what happens to the money

Powerball winner scoops $1.817 billion jackpot on Christmas Eve, but nobody knows who they are yet

Borrowers who pay off or close their junior liens during the refinance avoid consent altogether. Those keeping a HELOC depend on the second-lien lender’s approval, combined loan-to-value limits, and processing backlogs.

“The subordination agreement has one simple purpose. It assigns your new mortgage to first lien position, making it possible to refinance with a home equity loan or line of credit,” — U.S. Bank explainer.

Moves that keep your refinance alive when consent is required

Act before you lock. Many servicers quote 7–10 business days (and sometimes longer) to process subordination, and some charge a recording or processing fee. Build that timing into your closing plan.

| Step | Detail | Deadline |

|---|---|---|

| 1 | Pull title and list all junior liens (HELOC, seconds, DPA). Confirm CLTV meets the new lender’s cap. | Week 1 |

| 2 | Request the subordination checklist and fee quote from your junior-lien servicer; assemble note, payoff, and new loan terms. | Within 3 business days |

| 3 | Time the rate: consider a longer lock or float until subordination is approved to avoid lock-expiration costs. | Before rate lock |

| 4 | Reduce risk factors: temporarily freeze or close a zero-balance HELOC or pay down to meet CLTV if required. | Before underwriting final |

Typical quoted timelines range from ~10 business days for straightforward files to 20–30+ days in agency or high-volume pipelines. Build cushions into your purchase of rate-lock duration.

What could stall you in the next 30–90 days if rates dip again

Another rate slide can trigger a wave of refinance files and subordination backlogs, stretching approvals from 10 days toward 30–60+ days. Plan for a slower turn if you submit between now and December 24, 2025.

Agency programs and servicer rules may also restrict subordination on certain cash-out scenarios or require extra docs, adding days to the timeline.

Are more lenders refusing to subordinate as CLTVs creep higher?

Some lenders will not resubordinate if the combined loan-to-value ratio edges above their comfort band or if terms materially increase their risk. If your HELOC limit pushes CLTV too high, your options may be to pay it down, close it, or roll it into the new first mortgage.

SOURCES

- https://selling-guide.fanniemae.com/sel/b2-1.2-04/subordinate-financing

- https://www.usbank.com/financialiq/manage-your-household/manage-debt/whats-a-subordination-agreement-why-it-matters.html

- https://sf.gov/refinancing-and-subordination

Jessica Morrison is a seasoned entertainment writer with over a decade of experience covering television, film, and pop culture. After earning a degree in journalism from New York University, she worked as a freelance writer for various entertainment magazines before joining red94.net. Her expertise lies in analyzing television series, from groundbreaking dramas to light-hearted comedies, and she often provides in-depth reviews and industry insights. Outside of writing, Jessica is an avid film buff and enjoys discovering new indie movies at local festivals.

So, picture this: youre all set for that refinance, feeling like a financial guru, and bam! That sneaky consent clause pops up out of nowhere. Ever had that happen? Its like finding a hidden boss level in a game. Tricky, right?

Man, that sneaky consent clause is like a surprise plot twist in a movie you thought you had all figured out. Its like thinking youre about to win the game, and suddenly, the rules change on you. Tricky indeed. Have you found any clever ways to navigate those unexpected financial hurdles? Share your secret strategies!

Remember when you thought refinancing was a walk in the park? Watch out for that sneaky consent clause that can trip you up! Got any horror stories to share about unexpected refi roadblocks?

Remember that time I almost missed out on refinancing because of some sneaky clause? Crazy how one little detail can mess it all up. Always check the fine print, folks. Got any close calls with tricky clauses?

Remember that time I thought Id breeze through a refinance? Then bam! That sneaky consent clause shows up. Always read the fine print, folks! Ever had a clause catch you off guard?

I feel you, mate! Those sneaky clauses can be real troublemakers, popping up when you least expect it. Story time: I once signed up for a gym membership, thinking it was all smooth sailing until I discovered a hidden fee buried in the contract. Sneaky, right? Have you ever had a similar clause ambush you when you were least prepared? Just goes to show, the fine print can be a real minefield!

Remember that time I almost missed out on refinancing because of some sneaky clause? Always read the fine print, folks. You never know what might trip you up! Ever had a close call like that?

You ever read those tiny clauses? One wrong word, and bam, your refinance is toast. Sneaky banks! Whats your worst fine-print horror story?

Oh, those sneaky banks with their fine print traps! I once signed up for a credit card thinking I was getting a great deal, only to discover buried in the fine print that the interest rate would skyrocket after just a few months. It was like a financial rollercoaster I never wanted to ride! Have you ever had a similar heart-stopping moment with the fine print? Its like theyre playing a game of financial hide-and-seek with us!

Remember when I tried to refinance, and suddenly, they hit me with this sneaky consent clause? Its like finding a hidden pickle in your sandwich! Sneaky banks… Got any tips to navigate this mess next time?

Man, those sneaky consent clauses are like a ninja move from the banks, right? Its as surprising as finding a hidden pickle in your sandwich! Next time, try arming yourself with some fine print magnifying glasses, a lawyer on speed dial, and a pinch of skepticism. But hey, who knows what other surprises those banks have up their sleeves, right? How do you plan to outsmart them next time? Maybe a secret handshake or a decoder ring could come in handy? Just kidding… or am I?